Every year, thousands of F&O traders file their ITR and move on. They trust their consultant. They assume someone checked the numbers. They have no idea what is coming.

AY 2026-27 just changed the game. And if your consultant has not told you about it yet — that silence is the problem.

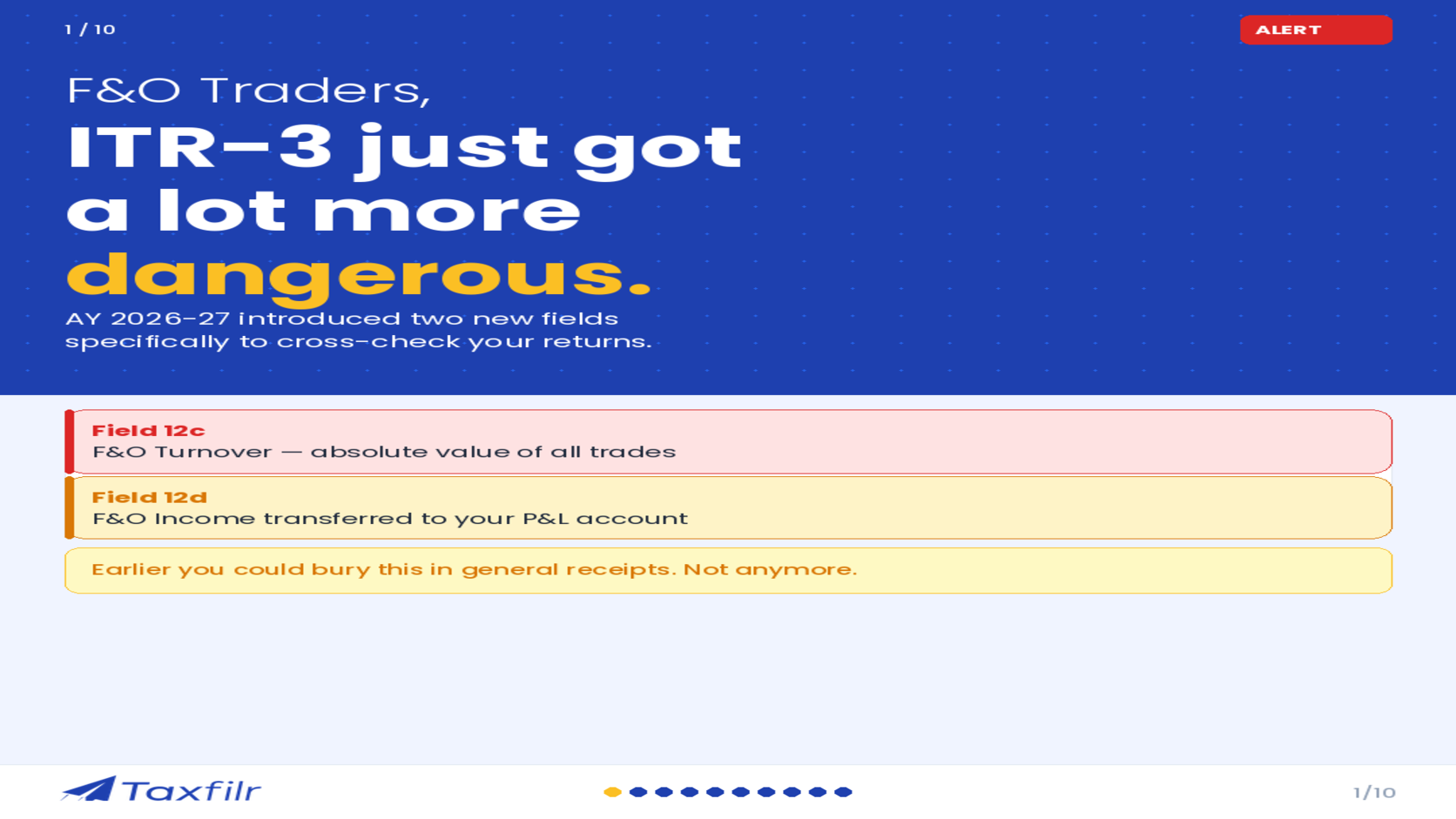

Two new fields. One very big shift.

The Income Tax Department has introduced two mandatory new fields in ITR-3 specifically for F&O traders:

Field 12c — F&O Turnover calculated using the absolute value method (ICAI)

Field 12d — F&O income or loss transferred to the P&L account

These fields are not optional. They are not a formality. They are a direct line into your trading activity — and they are automatically cross-checked against four separate data sources the moment you file:

→ Your broker's P&L statement

→ Your AIS and TIS data on the IT portal

→ STT records from your transactions

→ NSE/BSE exchange reports

If any number does not match — across any of those four sources — a notice is generated. Automatically. No human intervention required.

What the IT Department is looking for

Here is the scenario they are specifically designed to flag:

F&O turnover declared: ₹50,00,000

Taxable income declared: ₹12,000

That mismatch is now machine-readable. An AI flags it the moment your return is processed. There is no longer a grey area where a large turnover and a suspiciously small income can quietly coexist in the same ITR.

The window for "I didn't know" is closing fast.

Three things every F&O trader must know right now

1. Turnover is not your net profit

This is the most common and most expensive mistake I see. F&O turnover under the ICAI absolute value method is the sum of the absolute value of every trade result — every profit AND every loss, counted separately.

If you made ₹28,000 on one trade and lost ₹15,000 on another, your turnover is ₹43,000. Not ₹13,000. Not zero.

For options specifically, the full sale consideration counts as turnover — not just the net gain. This is why options traders regularly show crore-level turnover on what feels like small capital. And it is why getting this number wrong in Field 12c triggers an immediate flag.

2. Section 44AD does not apply to F&O income

Presumptive taxation — where you declare 8% of turnover as profit and file ITR-4 without maintaining detailed books — is completely unavailable to F&O traders.

F&O income is business income. It requires ITR-3. It requires full books of account — a trading log, a ledger, a complete P&L. If your turnover crosses ₹10 crore, or if your declared profit is below 8% of turnover, a tax audit becomes mandatory.

If your consultant filed you on ITR-4 last year, that is a problem worth examining immediately.

3. Your books must match your broker's data — before you file, not after

The IT Department is not waiting for a human to spot the discrepancy. The cross-check between Field 12c, your AIS, your broker P&L, and the STT records happens on submission. Reconciling after a notice arrives is far more expensive — in time, money, and anxiety — than reconciling before you file.

The question I want every trader to sit with

Your ITR can be scrutinised for up to ten years after filing. Assessments can be reopened. Notices can arrive long after you have forgotten the return even existed.

When that happens — when the IT Department writes to you eighteen months from now — will your consultant still be reachable? Will they stand behind what they filed? Will they respond on your behalf, represent your case, and make it right if something was wrong?

Or will you be sitting alone with a notice, a penalty order, and a WhatsApp number that no longer replies?

What responsible F&O filing actually looks like

At Taxfilr, every F&O return we file goes through the following before submission:

✅ Turnover calculated using the ICAI absolute value method

✅ Fields 12c and 12d verified and filled accurately

✅ Broker P&L reconciled with AIS and Form 26AS

✅ All deductions verified against actual documents

✅ CA-reviewed ITR-3 filing — not self-filed, not auto-generated

✅ Full notice support if you receive one — we respond, we represent

We have been doing this since 2009. We are not a ₹999 app. We are a professional practice that stands behind every return it files — for as long as it can be questioned.

If you trade F&O, do these three things this week:

→ Pull your broker's complete P&L report for FY 2025-26

→ Cross-check it line by line against your AIS on the IT portal

→ File with a CA who understands derivatives taxation — not someone who promises the maximum refund before seeing a single document

The ITR-3 deadline for AY 2026-27 is July 31, 2026. The time to prepare is now — not the week before.

If you found this useful, share it with an F&O trader in your network. The traders who get notices in October are almost always the ones who were never warned in June.